5 Ways Your Tax Refund Can Help You Buy Your First Home

*

If you're expecting a refund this year, instead of spending it on

things that you don’t need, consider using it to invest in your future!

things that you don’t need, consider using it to invest in your future!

What better way to do so than using your tax refund as a

down payment on the home of your dreams!

down payment on the home of your dreams!

Consult a professional Tax Advisor & Preparer like

CLAY TAX SERVICES to help you maximize your refund amount.

*

Check out these 5 ways that your tax refund can help bring

you closer to homeownership:

you closer to homeownership:

*

1. Save for a down payment.

Saving for a down payment can be one of the biggest

barriers to homeownership.

barriers to homeownership.

When you get your tax refund, put it in a savings account at your bank

to build up a deposit fund. Keep adding to the fund until you have a min

of 5% of the total cost of the home you wish to purchase.

to build up a deposit fund. Keep adding to the fund until you have a min

of 5% of the total cost of the home you wish to purchase.

Today's homebuyers tend to underestimate the size of the down

payment they need. Depending on your credit history, score and other factors,

many borrowers can make a down payment of about 3 to 20%

— depending on the type of loan you choose & the condition of the

home you choose.

payment they need. Depending on your credit history, score and other factors,

many borrowers can make a down payment of about 3 to 20%

— depending on the type of loan you choose & the condition of the

home you choose.

Whether if it's move-in ready or a fixer-upper, there are a variety

of programs & products to assist you in the home buying process.

of programs & products to assist you in the home buying process.

With Freddie Mac's 3% down mortgage –

Home Possible Advantage®–qualified borrowers could make a

down payment of as little as $6,000 for a $200,000 home.

Home Possible Advantage®–qualified borrowers could make a

down payment of as little as $6,000 for a $200,000 home.

&

With IHDA Forgivable Mortgage, homebuyers are given 4% of

the purchase price up to $6,000 in assistance for a down payment

& closing costs, forgiven monthly over 10 years –

it’s a gift that does not have to be repaid

the purchase price up to $6,000 in assistance for a down payment

& closing costs, forgiven monthly over 10 years –

it’s a gift that does not have to be repaid

30-year, fixed-rate mortgage with an affordable interest rate.

Down payment assistance programs can also help you bridge

the cash gap. There are thousands of programs across the country

that can help you save on your down payment and closing costs.

A great place to start is right where you live.

the cash gap. There are thousands of programs across the country

that can help you save on your down payment and closing costs.

A great place to start is right where you live.

*

Many states, county, and city governments provide financial assistance

for people in their communities who are well qualified and ready for

homeownership. Check out the programs available in your market

and see if you are eligible.

for people in their communities who are well qualified and ready for

homeownership. Check out the programs available in your market

and see if you are eligible.

*

2. Pay for closing costs.

A homebuyer typically pays between about 2% and 5% of the home

purchase price in closing fees, but the amount varies.

purchase price in closing fees, but the amount varies.

Some closing costs that can be incurred when you’re buying a home are:

Attorney fees

Home Insurance

Appraisal and inspection fees

Escrow costs

Title insurance

Transfer Stamps

Your tax return can be a great way to help pay for these costs.

See your Loan Officer for the cost analysis.

3. Lower your interest rate.

You can pay discount points to buy down your mortgage interest rate.

A "point" equals one percent of the loan. It's essentially an upfront

interest payment to lock in a lower interest rate on your

fixed-rate mortgage. So, if you are borrowing $200,000,

paying one discount point would mean paying $2,000 upfront at closing —

but it may end up saving you more in interest payments over the life of the loan.

A "point" equals one percent of the loan. It's essentially an upfront

interest payment to lock in a lower interest rate on your

fixed-rate mortgage. So, if you are borrowing $200,000,

paying one discount point would mean paying $2,000 upfront at closing —

but it may end up saving you more in interest payments over the life of the loan.

4. Use It to Cover Moving Costs

At the end of the home buying process is the closing. This is where

the transferring of the older owner to you, the new owner takes place.

If the process goes smoothly (but sometimes it doesn’t )that means you’ve

done a great job of managing your finances, saving money and you had

a great team of professionals helping you along the journey like your

REAL ESTATE AGENT, LENDER & ATTORNEY!

the transferring of the older owner to you, the new owner takes place.

If the process goes smoothly (but sometimes it doesn’t )that means you’ve

done a great job of managing your finances, saving money and you had

a great team of professionals helping you along the journey like your

REAL ESTATE AGENT, LENDER & ATTORNEY!

Now its time to move & it’s possible that you’ll have moving

expenses to deal with, especially if you have been living in an apartment

or other rental spaces.

expenses to deal with, especially if you have been living in an apartment

or other rental spaces.

Your tax refund can help cover additional costs like:

Renting a moving truck

Purchasing packaging material

Paying off storage unit bill

Or paying the balance off from breaking a lease

5. Use It to Build Your Emergency Fund

Every homeowner should have an emergency fund. The same savings account

you used to save for the down payment can now serve a different purpose;

that is to cover several months of expenses, including your mortgage payment,

unexpected expenses, such as a major car repair, job loss, illness or

other income interruptions.

you used to save for the down payment can now serve a different purpose;

that is to cover several months of expenses, including your mortgage payment,

unexpected expenses, such as a major car repair, job loss, illness or

other income interruptions.

*

You could add your tax refund to your emergency fund to help protect you

from these financial crises if any arises.

from these financial crises if any arises.

*

These are just a few of the ways that you can put your tax refund to good use!

*

When you’re ready to start your home-buying process,

Call me today and Let's set up a plan to get you to your GOAL &

talk about how my Real Estate Services can help you ACHIEVE it!

talk about how my Real Estate Services can help you ACHIEVE it!

*

At Prestige Partners Realty, we pride ourselves in delivering you a

Smooth, Thorough & Professional home-buying process from start to finish!

Smooth, Thorough & Professional home-buying process from start to finish!

We have an AWESOME Networking Team of THE BEST

experts in their fields to assist us in making

YOUR DREAM of HOMEOWNERSHIP A REALITY! 🔑🏡💯👍

SO WHOSE NEXT?

LET'S MAKE 2024

THE YEAR YOU BECOME A NEW HOMEOWNER OR INVESTOR!

THE YEAR YOU BECOME A NEW HOMEOWNER OR INVESTOR!

🏡❤

Julie K.

Prestige Partners Realty

(312)898-6545

SUBSCRIBE

▶

BOOKMARK-

▶

SHARE

▶

VISIT

www.JulieKCreativeLiving.com for Help with Your Income Taxes Visit

https://claytaxservice.com/

Check Your Free Credit Report Before The End Of The Year

If you have been following my articles on repairing credit &

buying your first home, then you are already ahead of the crowd who has been

procrastinating with taking charge of their financial health.

buying your first home, then you are already ahead of the crowd who has been

procrastinating with taking charge of their financial health.

In a previous article, I gave you a few easy & simplified steps on how to

request, dissect & correct your FREE ANNUAL CREDIT REPORT; so that you can be on the road to buying your first home

or investment property!

request, dissect & correct your FREE ANNUAL CREDIT REPORT; so that you can be on the road to buying your first home

or investment property!

So to get EVERYONE ready to shop for your 1st NEW HOME for

the upcoming year, you must

REQUEST YOUR CREDIT REPORT with FICO Scores, if you haven’t done so this year.

You should request from all 3 major credit bureaus;

(Equifax, Transunion & Experian).

the upcoming year, you must

REQUEST YOUR CREDIT REPORT with FICO Scores, if you haven’t done so this year.

You should request from all 3 major credit bureaus;

(Equifax, Transunion & Experian).

Checking over your credit reports each year is the best way to find

reporting errors and detect early signs of identity theft. Getting a jump start

by watching over your reports or having them professionally monitored and checking for fraud can save you money and future headaches.

reporting errors and detect early signs of identity theft. Getting a jump start

by watching over your reports or having them professionally monitored and checking for fraud can save you money and future headaches.

For example, you may stumble upon proof that someone is using your

credit or trying to steal your identity by finding a credit account in your

name that you don't even recognize, or you may find you have addresses you

have never lived at the listed on your reports.

credit or trying to steal your identity by finding a credit account in your

name that you don't even recognize, or you may find you have addresses you

have never lived at the listed on your reports.

There is no reason not to take this important step to protect yourself and gain

useful insight into your financial health.

useful insight into your financial health.

It's fairly common for credit reports to have errors. Mistakes can be something as

simple as an incorrect date reported for an account opening or

your name is misspelled. However, errors can also have a negative impact

on your score such as a loan balance is reported in a much higher

amount than what you actually owe, showing a late payment and you are

set up for autopay or an unauthorized account opened in your name as

stated previously.

simple as an incorrect date reported for an account opening or

your name is misspelled. However, errors can also have a negative impact

on your score such as a loan balance is reported in a much higher

amount than what you actually owe, showing a late payment and you are

set up for autopay or an unauthorized account opened in your name as

stated previously.

So if you’re going to get a mortgage, you'll likely need to improve your

credit score or maintain the Excellent status you have to qualify for

your home loan and the only way to do that is to

GET YOUR ANNUAL CREDIT REPORT.

credit score or maintain the Excellent status you have to qualify for

your home loan and the only way to do that is to

GET YOUR ANNUAL CREDIT REPORT.

Article

Julie K.

Broker & Family Realtor

New Home Buyers - You Can Do It!!!

7 Easy Steps to Buying Your New Home

First-time home buyers tend to find the process confusing. I know, because I get questions via email on a regular basis and I too was once a FIRST TIME HOME BUYER! So I’ve created this simple guide to walk you through the different steps in a typical home-buying process.

.

STEP 1. ANALYZE YOUR FINANCIAL HEALTH & JOB HISTORY

If you don't have a budget, a min 6-month emergency funds saved, a separate account used just for long-term savings or if your employment is short-term or low paying. You have to re-evaluate your financial health. Finances are crucial to you obtaining a home loan. Many new homebuyers never take these factors into consideration. Some may feel that the job is enough. Lenders want to see your recent bank statements, tax records, and 2-year minimum of employment (verification letters) as well as your credit reports. They want to see your spending & savings habits, and how much you make to see if you may need a co-borrower because your income is insufficient.

This step also will give you an idea of the type of house, area & the price you can afford,

STEP 2. CHECK YOUR CREDIT REPORT & SCORE

You can get a free report once a year through Annualcreditreport.com. The report pulls data from the three major credit-reporting agencies: Equifax, TransUnion, and Experian. You will need to check all three companies because they are individually operated & do not pass information about you to each other. If there are inaccuracies, be diligent in getting them off. Having erroneous items in your file can delay the process of buying your new home.

Based on your credit report, Fair Isaac & Co. (FICO) assigns you a credit score ranging from 350 to 850. The higher your credit score, the lower the interest rate on your mortgage & makes a difference when you are renting an apartment or a home.

Scores are based on:

• Payment history: Have you paid your bills on time?

• Amounts owed: What is your overall debt? What is your debt compared to how much you earn? Do you have the financial resources and means to repay your debts, including the mortgage loan?

(Note:) You have to keep your credit cards Under 30% utilization, so start paying them down.

• Length of credit history: Lenders like to see how long you have been borrowing

• Types of credit: Lenders like to see a variety of types such as bank cards, car loans, and student loans as well as rental payments. If your landlord offers credit reporting of your monthly rent, invest in it especially if you make your payment on a timely basis.

• New credit inquiries: Have you applied for new credit? How many inquiries have you made that is not associated with a tradeline? Applying for too many tradelines can impact your score by lowering by 2 points or more, especially if you were not approved by the credit grantor.

IF YOU ARE AN HONORABLY DISCHARGED VETERAN:

You may, can use your VA benefits and obtain a VA Loan without any down payment.

(conditions may apply) Visit

https://www.benefits.va.gov/BENEFITS/factsheets/homeloans/VA_Guaranteed_Home_Loans.pdf (To check your eligibility)

VA loans do not require a down payment, or any mortgage insurance. Unlike FHA, the VA does not impose a minimum credit score requirement. However, most lenders will want you to have a minimum credit score between 580-620 before approving the loan.

STEP 3. FIGURE OUT HOW MUCH (HOUSE) YOU CAN AFFORD

Once you have done steps 1 & 2, You can take your research to a Lender to get a pre-approval before you search for a home. If you were to skip the pre-approval and go straight into the house-hunting process, you might end up wasting time by looking at homes that are above your price range. Most Realtor will require you to have a pre-approval before they start taking you out to look at homes.

The Lender will give you an approximate amount but that doesn't mean you have to use the total amount. Remember the higher the price of a home the higher your mortgage and look out for high taxes, which is not figured into your pre-approval amount. The higher the taxes, the less buying power you will have. You will have an opportunity to apply for a Homeowner's exemption being the home is your principal residence. ( check your local assessor's office) Normally a new homeowner can apply at the beginning of a new year but will have to pay the higher tax until that time. If your taxes are too high for the amount of income you bring in, a lender may reject your contract.

To give yourself a look into how much mortgage you can afford, use the mortgage calculator :

STEP 4. MAKE A PLAN & SET YOUR GOALS

By now you have some knowledge of finances, credit, and mortgages. Let's begin to execute a plan of action & set some time frame to buy your NEW HOME!

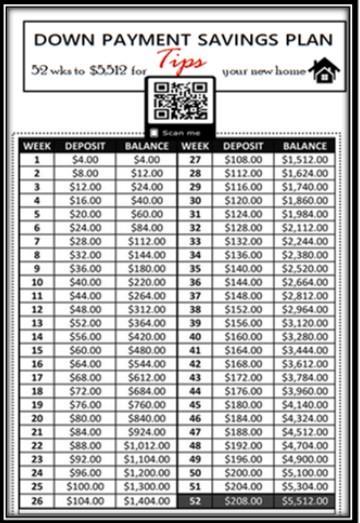

4a. Open a separate bank account used for your down payment & closing costs. (Credit Unions are great especially if you buy in an area where they service) Use my Quick Tip Savings Plan to start stacking your cash

4b. Be Realistic & Patient with your savings plan. This chart can be modified to fit your personal income & lifestyle. These figures are based on you saving for 1 yr. If you want to move sooner, you can double the amount & create a 6-month plan. It's all up to you. there is no right or wrong way to save.

4c. Gather all three credit reports & compare them side-by-side making sure all erroneous & inaccurate information is removed. Know your credit score! You may have to pay a small fee to get all three of your scores but it is well worth it. Think of it as an investment! Knowing your score gives you a picture of what you must do to get to the point of the lender's approval.

4d. Pay down debt & don't spend no more than 30% of your credit card limit.

4e. If you MUST open a credit card (tradeline) to rebuild your credit file or establish one, get a secured one with a small limit like $300-500 where you can make a security deposit to the grantor & they give you that amount in credit. They will report monthly so only buy something small, remember to only use 30% or less of the card's limit; pay on it monthly & watch your score go up!

4f. Start budgeting your money & making cuts.

My story

I remember when I was renting from family & just being upset with asking all the time for just general repairs to be done for the money I was paying.

*

I did the same thing many of you have done, (total up my monthly rental payments) It just blew me away how much I gave away to my landlord!💸

So even though I had to pay rent every month it was IMPERATIVE that I consider saving money for my DOWN PAYMENT & CLOSING COSTS for my own home🏡 & build my own EQUITY.

I was 28 at the time & my goal was to build up & clean my credit file, open a separate savings account with a Different Bank & deposit money for my new house & set a deadline of being A HOMEOWNER before I was 30 years old.

*

I did it! 😀 It was hard at times but I kept focusing on my home & the freedom/security I wanted.

*

I made up a REALISTIC BUDGET; PINCHED my pennies & ✂cut stuff out like

✔💅nail shop expense

✔👗👜👠👑🛍clothing & shoe shopping sprees

✔☕Cut out My DELICIOUS STARBUCKS Everyday😭😭😭

✔ Eating out @ restaurants 🍽🍕🌮🍟🍔🍗🍸🍳🍦

✔ Entertainment & Costly Vacations🎷🎶🎺🎵🎬🎭✈🛳🏖

^

NOW ADD THOSE ITEMS UP! What a huge Savings!!!!💯💰

*

You will be floored to see where your hard-earned money is going & HOW MUCH YOU'RE REALLY SPENDING💸😣 on "STUFF" that won't improve your financial health nor help create GENERATIONAL WEALTH for you & your kids.

I still keep my financial mindset of saving where I can; still to this day & it's been over 20 years since I've been in my home, that's getting ready to be paid off soon! (made extra payments toward my principal amount owed, with the money being saved)

I still coupon, go to movies on $5 Tuesdays, Cook @ home, Thrift shop, do my own hair & nails, use Groupon, Living Social & other discount sites to find deals

(splurge every now & then)😆

4g. Consult with a lender when you get ready as explained in Step 1. Make sure you do your preparation. Have in hand your 2-3 months of bank statements of your new bank acct., 2yrs of W2s & paycheck stubs, if you are an independent contractor you need your profit & loss statement & 1099 for the last 2 years., any Divorce decree if recently divorced showing alimony or child support, if you are currently renting, your last 12 rent payments & landlords for the past 2 yrs; And if you are a US Veteran, check your Benefit Eligibility status.

https://www.benefits.va.gov/BENEFITS/factsheets/homeloans/VA_Guaranteed_Home_Loans.pdf ( To check your eligibility)

STEP 5. HIRE A REAL ESTATE ATTORNEY

Representation is important as you will need an experienced attorney who specializes in Real Estate Law. You will put yourself at a great disadvantage by NOT having the proper attorney or none at all. The attorney has your best interest at all times. He will help you navigate the pre & post-closing process. The attorney will make sure that your contract is written & structured to meet your individual needs and if there is a conflict, he is the powerhouse to get things back on track!

STEP 6. FIND A REALTOR

Now it's time to go Home Shopping. Finding the right Realtor is just as important as finding the Right Home! Real Estate Brokers have a wealth of information and Networking contacts of Lenders, Attorneys, Contractors, Handymen, and other pertinent people you will need during the process.

However, all agents are not created equal so do your due diligence. Ask for referrals from family & friends or go to www.Realtor.com to find your Agent.

You should feel good when you are with your Agent. While buying a new home one can expect some nervous jitters but that goes with the territory. Your agent is there to help educate you in the process, ease your mind in the decision-making/negotiating process & show you the homes based on the pre-approval & your personal preferences.

If you have a busy or irregular schedule, your Real Estate Agent should work with you to accommodate any scheduling conflicts whether if the Agent is full-time or part-time.

Communication is a key factor, as both you the buyer & agent should be speaking on a regular during the process.

Although with modern telephone technology, texting & email are the main sources of communication and things can get lost in translation & misconstrued, don't ever discount a good verbal phone conversation that can quickly clear things up.

THANK YOU to all of my clients & networking business partners to whom I had the great pleasure of servicing all YOUR REAL ESTATE NEEDS.

As Your Family Realtor, you can still expect from me, quality professional, dynamic customer service to assist your needs or concerns during the real estate transactions.

Being a Powerhouse Broker, backed by a Strong Experienced Team & Support Systems, my clients are led seamlessly through the Real Estate process with unmatched market knowledge, dependability, and responsiveness unlike no other.

Special attention to detail along with high standards and integrity are key elements that I deliver to all my clientele; whether you are a first-time homebuyer, seller, seasoned, or a new investor.

So contact me TODAY! Let's talk about how my Real Estate Services can help you!

I am YOUR FAMILY REALTOR Today, Tomorrow & Always!

STEP 7. WELCOME TO YOUR FOREVER HOME!

After the home was selected, you put in an offer that was accepted & locked it in with your earnest money; everything from inspections to appraisals & underwriting to CLEAR TO CLOSE, then finally closing!

Congratulations!!! Get your keys and move in!

If You Have a Low to Moderate Income, Discover the Possibilities With Home Possible®

This Freddie Mac Program is breaking down the barriers to homeownership and raising hope for very low- to moderate-income borrowers. The Freddie Mac Home Possible® mortgage offers more options and credit flexibilities than ever before to help very low-to-moderate-income borrowers attain the dream of owning a home!

You can buy 1-4 units, condos and planned-unit developments; manufactured homes are eligible with certain restrictions.

Contact me TODAY! Let's talk about how my Real Estate Services can help you!

I am YOUR FAMILY REALTOR Today, Tomorrow & Always

Julie K., Broker

You can buy 1-4 units, condos and planned-unit developments; manufactured homes are eligible with certain restrictions.

Contact me TODAY! Let's talk about how my Real Estate Services can help you!

I am YOUR FAMILY REALTOR Today, Tomorrow & Always

Julie K., Broker

Prestige Partners Realty

No comments:

Post a Comment